Could Earthquakes in Turkey Lead to Revivification and Revitalization?

We predict a negative effect on Turkey due to the recent disaster along its southern borders, but this will be limited and manageable.

March 3, 2023

C

ould earthquakes, including those in Turkey, lead to a new course of revivification and revitalization?

Scientists and economists alike seem to agree on the short-term negative economic impacts of natural disasters such as earthquakes. However, the longer-term reflections are not clear since the long-term growth and GDP impacts could even be positive as disaster-hit regions usually grow faster in order to catch up with other regions. National and international support further facilitate this process.

Extensive literature also demonstrates that new investments, government expenditures, and other support packages may lead to significant long-term positive effects on the GDP. For example, literature shows that while the short-term impacts of big natural disasters could be negative (-0.9 percent on average), the longer-term effects turn positive (0.6 percent on average).

During the next few months, we predict a negative effect on Turkey due to the recent disaster along its southern borders, but this will be limited and manageable. Starting from the second half of 2023, economic activity should recover and growth should once again gain momentum.

A better picture of this regeneration course is only possible through a snapshot of the regional economy. TÜİK (Turkish Statistical Institute) data shows that around 14 million people, more than 16 percent of the population, have been adversely affected by the recent earthquakes. The earthquake hit regional economy is predominantly dependent on the food, agriculture, steel production, energy, cement, textile, and clothing industries.

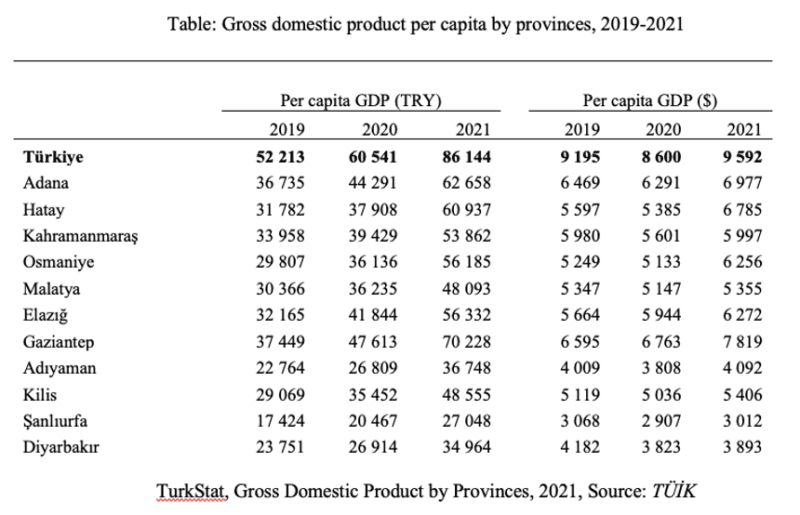

This eleven earthquake-stricken provinces have a relatively smaller GDP per capita, specifically about two-thirds of the national average. However, they represent a little less than one percent of the growth figure in Turkey, according to TÜİK. These GDP contributions are not expected to drop to nothing right away but should decelerate significantly.

Meanwhile, the hardest-hit Turkish provinces constitute 10 percent of the Turkish economy with Gaziantep, Adana, and Hatay being the three biggest economies of the 11. Fifteen percent of total agricultural production, 11 percent of industrial production, and 11 percent of manufacturing production are based in these 11 provinces.

All together the exports of the 11 provinces are about nine percent of the total Turkish exports while 21 percent of Turkey’s crop production, 12 percent of grain and other crops, 17 percent of farmable land, 12 percent of cattle, and 16 percent of small livestock can be found in these 11 provinces.

The total rebuilding cost estimate following these earthquakes is approximately $45-$80 billion, with a mean estimate of $60 billion. This figure includes growth decline, the cost of moving the rubble, the cost of reconstruction and renovation of the houses, labor and human capital losses, infrastructure and public facilities cost, as well as education and human capital losses.

The full scale of the economic costs is yet unknown. Indeed, earthquake cost estimation is a difficult endeavor, and considering the earlier mixed figures of destruction and the usual complexity of estimation, we reason these costs could potentially be expanded to a $40-$150 billion interval.

However, the physical construction cost alone is estimated to be as low as $15-$30 billion. This is, of course, assuming the land is provided by the Turkish Treasury or that it belongs to the existing landlords.

The dynamic Turkish economy, national and international financial support, strong fundamentals, and the economic structure of the region are all likely to mitigate the negative impacts. For example, investment bank Goldman Sachs, the World Bank and IMF have all predicted a minimum impact to the GDP and growth figures.

Goldman Sachs cites an earlier paper showing a 1.2 percent effect on the Turkish economy following the 1999 Marmara earthquake, and reasons that the impact of the latest earthquake could be much more limited. It should be kept in mind that the Marmara and Düzce earthquakes of 1999 affected an area corresponding to almost 35 percent of the Turkish GDP and 47 percent of the industrial production at the time.

Like these institutions, we, too, do not expect effects similar in scale to the 1999 earthquake. The earthquake struck southern Turkey this time is not in the industrial heartland, and therefore, economic costs, financial, fiscal, trade, inflationary and growth reflections should all be limited.

Despite all the negative implications, for example, the capital stock damages due to the tremblor do not show up in the national GDP; however, new (public and private) investments to rebuilt the capital stock are part of the GDP, making this a positive post-earthquake investment effect. Ta (2022) demonstrates empirical evidence that post-earthquake firm investments could increase by more than 2 percent and that the real economic growth would also be relatively higher.

There is also another line of research that discusses the positive “creative destruction” impacts following natural disasters. These destructive disasters, the literature underlines, can lead to new technologies, higher productivity, and hence much higher growth rates in the disaster-hit areas. Xiao’s (2011) “correction impact” argument, in particular, is noteworthy at this point.

In certain cases where the Keynesian multiplier of expenditures is proven relatively higher – as in dynamic economies such as Turkey – shortly after the disasters, the national GDP could actually revive rather than contract as a result of rising expenditures and the demand effect.

Natural disasters could also lead to higher labor supply and more incentive to work longer hours, in an effort to maintain the quality of life or standards of living. This, in return, would lead to higher output or production effect. The demand would also bounce back, and the resulting profit opportunities would increase production as well.

The reconstruction and new investment efforts by public institutions and the private sector can further boost economic activity. Foreign capital inflow, financial support, new public incentives, government expenditure to rebuilt houses, new infrastructure investment, and business incentives could all boost economic activity and end economic stagnation.

Turkey has already created a resilient economy and a strong infrastructure to deal with such catastrophes. The dynamic Turkish economy will likely recover from the devastation of these earthquakes quickly. And most importantly – at least theoretically – Turkey has also learned its lesson from the 1999 Marmara earthquake.

Turkey has extensive experience in dealing with natural disasters, including earthquakes. Raschky (2008) has shown that the latter matters as institutional quality and practical experiences are extremely important in mitigating the disaster costs. Earlier wildfires, floods, and other disasters as well as regional wars, climate change, and the long-standing PKK terror attacks have all been dealt with thanks to Turkey’s strong institutional structures, its dynamic economy, and strong social and human capital.

Transportation infrastructure including highways, airports, railways, and seaports that connect earthquake-hit cities to the rest of the country and to the world should be renovated soon. Bilateral and multilateral agreements with international and national financial institutions should be signed to ensure funding for regional and local producers, and the commercial entities. The most critical issue here is probably financing the regional infrastructure. Medium-to-longer-term financing options are pivotal for these types of physical investments.

Infrastructure investments, the construction sector, energy, and agricultural subsidies along with a huge external and domestic capital inflow towards this region could help boost the regional economy in the short-to-medium run. Rebuilding these cities, and reactivating the regional economy and its potential may also lead to longer-term higher multiplier effects for the national economy.

Recommended

Following the February 6 earthquakes, slower and stagnant economic activity or even an economic contraction can be expected; however, in a few months, an accelerated economic recovery should follow. The Marmara earthquake’s estimated cost on GDP growth rate was predicted to be -1 percent in 1999 and +1.5 percent in 2000; starting in late 1999, rebuilding expenditures by the government had a rapid positive impact on growth.

In the past 20 years of the AK (Justice and Development) Party governments, Turkey has built a very strong economic foundation and strong infrastructure. Massive infrastructure programs including new airports, railways, tunnels, ports, roads, giant city hospitals, regional universities, and sizeable state-supported social housing projects (by TOKİ) are all part of these strong fundamentals.

The production base of the Turkish economy is also strong. Almost everything for the rescue, relief, and reconstruction processes can be and, as a matter of fact, is being produced in Turkey nowadays.

Turkey is much stronger, today, than it was back in 1999. It has a much stronger production capacity. Infrastructure, logistics, and transportation investments over the past 20 years of political stability in Turkey have paved the way for a much stronger, confident, resilient, and operational economy and institutional structure.

Reactivated social capital is already a very critical issue. More importantly, production capacity, human capital base, new investments, and inflow of financial capital should all be expected to help rebuild the region’s physical infrastructure, revive weak business life, and boost the regional economy.

*All calculations unless otherwise indicated are by the author.

Dr. Bagis has a multidisciplinary B.Sc. from ITU (2006), an Economics M.A. from Sabanci University (2009) and a Ph.D. in Economics from the University of California (2014). In addition to his academic career, he has had private sector experiences at various international and domestic companies and institutions. He has taught graduate and undergraduate level economics, math and finance courses at prominent universities including University of California Berkeley and Sabanci University. His analysis and working papers are published by various prominent institutions including SETA and SAM.

You can see how this popup was set up in our step-by-step guide: https://wppopupmaker.com/guides/auto-opening-announcement-popups/

![]()

Stay informed by subscribing to

our weekly newsletter.

You can see how this popup was set up in our step-by-step guide: https://wppopupmaker.com/guides/auto-opening-announcement-popups/

You can see how this popup was set up in our step-by-step guide: https://wppopupmaker.com/guides/auto-opening-announcement-popups/

You can see how this popup was set up in our step-by-step guide: https://wppopupmaker.com/guides/auto-opening-announcement-popups/

You can see how this popup was set up in our step-by-step guide: https://wppopupmaker.com/guides/auto-opening-announcement-popups/