There seems to be no universally applicable definition of a sovereign wealth fund (SWF), and the SWF industry is made up of a heterogeneous class of funds, often shaped by the individual needs and conditions of the originating countries. However, against the background of the existing funds that are widely classified as SWFs, a sovereign wealth fund can be defined as an investment fund where:

- The asset owner is a sovereign government,

- It is managed professionally (either in-house or out-sourced) and independently of other government institutions,

- Its governance structure is well defined and partially transparent in that it reports either to the finance ministry or directly to the prime ministry,

- It has no or very few direct financial liabilities such as pension obligations,

- It invests in a wide range of financial and real assets for long-term financial return.

The source of capital for a SWF is typically one or more of the following national assets:

- Commodity revenues such as oil and gas exports

- Excess foreign exchange reserves and budget contributions

- State-owned or state-controlled real and financial assets

Historically, SWFs may have been founded for diverse purposes but the current SWF landscape seems to cover the following as purposes of SWFs: 1) “Stabilization” and reserve management (that include fiscal stabilization by managing investments of budget and trade surpluses, financial price stabilization through market-making against disruptive cross-border money flows and excess volatility in financial markets, and management of excess reserves at central banks, where excess means beyond the amount needed for monetary policy and stabilization), 2) growth of equity capital and markets through management of “savings” for inter-generational wealth transfer, 3) and finally economic “development” through investment in strategic sectors and assets.

Among many, the IMF’s definition of SWFs is closest to the above definition. According to the IMF, there are five categories of SWFs: 1) stabilization fund; 2) savings fund; 3) development fund; 4) pension reserve fund, and 5) reserve investment company. However, these categories need not be mutually exclusive.

History and Market Size

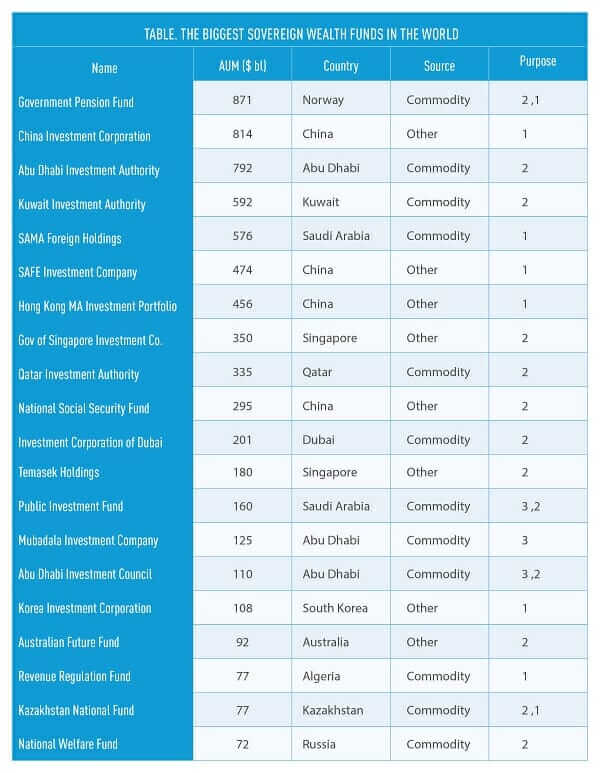

While SWFs have existed since 1970s, the SWF industry has grown considerably only after early 2000s. During the period, total assets under management (AUM) by SWFs have grown from less than $1 trillion before 2000 to about $7.4 trillion in 2015 and about two-thirds of the 78 SWFs today have been established since 2000. As such, the growing importance of SWFs is a relatively new phenomenon. Today, the current value of AUM can be estimated at around $7.8 trillion and it is expected to grow considerably in the foreseeable future. More than 80% of total AUM are held by the biggest 10 SWFs, most of which originate from emerging markets. The biggest SWFs (AUM, country of origin, source of capital, purpose) are shown in the following table:

Despite the fast growth, SWFs make up only about 7-8% of total AUM by institutional investors. As of 2015, the value of AUM globally is roughly estimated as $117 trillion with $100 trillion in conventional funds (39 in pension, 30 in insurance, and 30 in mutual funds) and $16 trillion in alternative funds (7.4 in SWF, 4 in private equity, 2.4 in hedge funds, 2.6 in ETFs, and others). These figures exclude privately managed private wealth. AUM under SWFs is more than the sum of private equity and hedge funds but still make up a small portion of the total fund industry. For reasons to be mentioned below, the share of SWFs is expected to increase in the future.