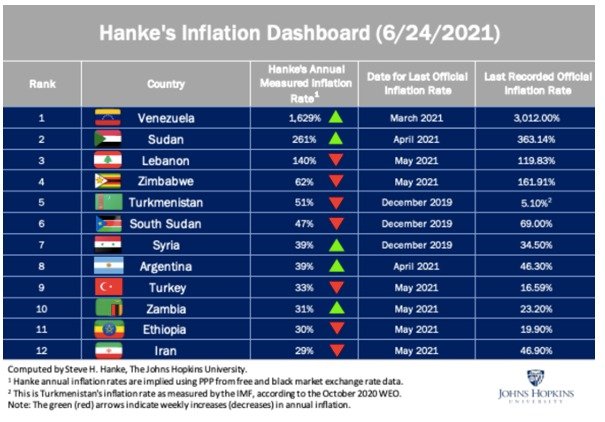

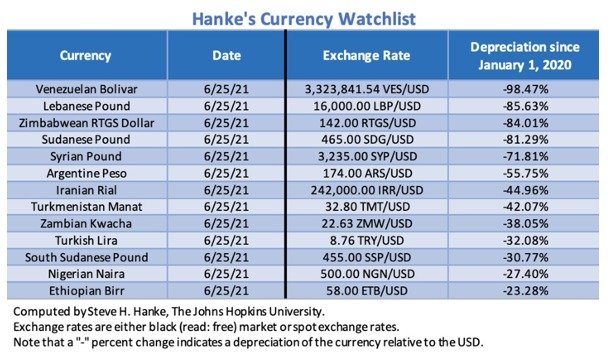

The transitional government has been facing shortages of foreign reserves, so without USD or EUR to back the Sudanese Pound, the market has lost confidence. This creates an inflationary spiral, and the inability to purchase goods such as fuel, food, and medicine (or service over 49 billion euros of foreign debt) is a huge anchor weighing down growth. It just takes one incident (on purpose or by accident) to set off a chain of events that can’t be contained, leading to more unrest, especially with the backdrop of a pandemic.

Emerging Markets are struggling under the weight of COVID19 and a sputtering global economy that is trying to awaken. The poor are getting poorer, and the middle class is being pushed closer to the poverty line as quality of life around the world is diminished. During COVID19, hundreds of millions of people fell out of the “Middle Class” and the $1.90 a day poverty line has only grown. This causes local populaces to become disenfranchised, resulting in more protests and riots against existing governments.

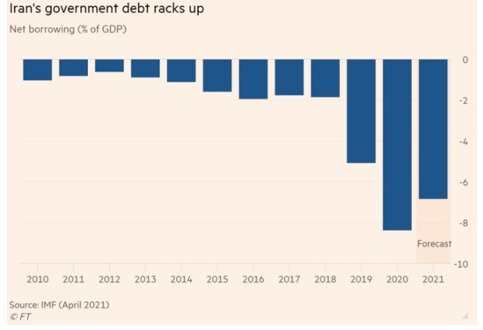

As COVID19 passes and people feel the sting of inflation and unemployment, pressure will mount on governments, and calls for change will rise. Each of the three governments discussed—Sudan: Transitional and Struggling, Lebanon: Fractured and Distrusted, Iran: Repressive and Suspected—will be under additional duress given the lack of local support, mounting debt, and failed policies.

The shortage of necessities (food, medicine, electricity, and fuel) will make it difficult to grow, and put more pressure on local governments. We have already seen food riots and protests . . . and we aren’t even fully out of the pandemic. Pain, despair, and anger has been bubbling beneath the surface for years, and now the match has been lit.