The US and China Semiconductor Rivalry: What Are the Stakes?

The US sanctions will further push China to focus on developing its own semiconductors—this may take time, but it is not impossible.

October 3, 2022

T

he rivalry between the U.S. and China, especially in the field of technology, gains further momentum. China aims to leapfrog the U.S. as tech leader, while the U.S. strives to maintain its leading position as the self-anointed world hegemon. Semiconductors, being a part of national security, play a critical role as an essential component of today’s economy and in the U.S. and China competition.

Affected by the Coronavirus pandemic, the world faced an unpreceded disruption in the semiconductor supply chain, which affected the automotive and high-tech consumer industries most, including defense industries. During the lockdown period, the demand for electronics skyrocketed and brought the semiconductor industry’s underlying problems, chiefly insufficient manufacturing capacity, to the fore.

The semiconductor industry has become a significant worldwide industry with a massive impact on the global economy. Semiconductors are among the most traded products in the world, alongside automobiles and refined petroleum. The industry has constantly increased in the previous years and according to the latest data the market reached a total of $555.9 billion in 2021. In is also estimated that semiconductor sales will reach $633 billion and $662 billion in 2022 and 2023 respectively.

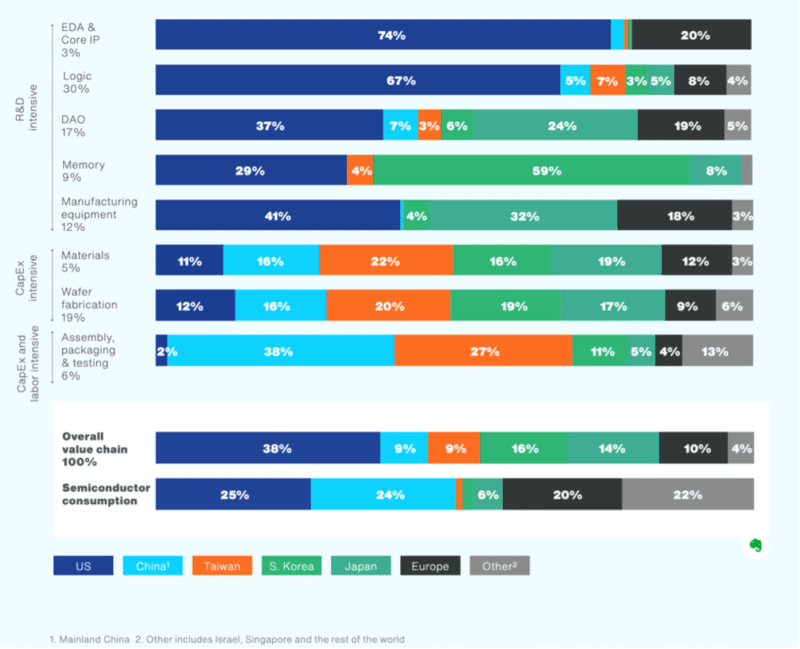

Except for a short period of time from 1985 to 1997, the U.S. has always dominated the global market share. In 2021, the U.S. accounted for 46% of the global semiconductor market shares, followed by South Korea with only 21%. Japan and the European Union cover 9% of the market each, while Taiwan and China maintain 8% and 7% respectively.

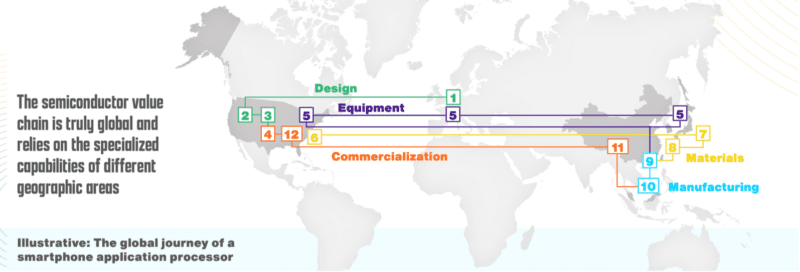

Even though the U.S. dominates the semiconductor market, the industry is not highly depended on the former. On the contrary, the semiconductor value chain is divided among several states and regions, which cover different parts of the chain based on their specialization, known as geographic specialization. (Fig. 1) This has created a great interdependence among the actors included in the chain. As a result, for a better understanding of the U.S. policies and their impact on the rivalry between the U.S. and China, one needs to understand how this value chain works.

The U.S. dominates the R&D-intensive activities which are related directly to the semiconductor design and are among the most important parts of the semiconductor value chain. Manufacturing, on the other hand, is dominated by the East Asia region. Specifically, raw materials and wafer fabrication, the front-end manufacturing, are dominated by Taiwan, while China dominates the back-end manufacturing with assembly, packing, and testing.

The United States is responsible for approximately 10% of the produced semiconductors. It is important to highlight that the most advanced semiconductors (below 10 nm), which are crucial for the defense industry, are manufactured exclusively in Taiwan (92%) and South Korea (8%). Lastly, both the U.S. and China dominate semiconductor consumption. (Fig. 2)

While the U.S. is the leader in semiconductor design, it lacks in manufacturing capacity. In 1997, the U.S. accounted for 37% of semiconductor production; in 2019, this share had declined to only 12%. As a result, the U.S. has become even more depended on East Asia states for semiconductor production.

Furthermore, 90% of the semiconductors used by American companies and all the semiconductors in U.S. defense systems are produced in Taiwan. Thus, it can be easily understood why increasing the U.S. semiconductor production capacity has become a national security priority.

In one of his tweets about semiconductors, Biden stated, “Semiconductor chips are the building blocks of the modern economy – they power our smartphones and cars. And for years, manufacturing was sent overseas. For the sake of American jobs and our economy, we must make these at home.” Biden posted the tweet just before the CHIPS and Science Act of 2022 was about to be approved by the Senate in July 2022.

The U.S. leadership, for some time now, has been aware of the importance of the semiconductor industry, both economically and politically. Since his arrival to the White House, Biden has taken many steps for the reshoring of semiconductor manufacturing.

Recommended

The most two important steps have been the signing of the CHIPS and Science Act of 2022 on August 9, and at the beginning of September, when two niche chip designers in the U.S., Nvidia and AMD, were instructed to stop exporting flagship artificial intelligence chips to China. It is expected that the ban on exports will be extended soon to other companies such as KLA Corp, Lam Research Corp (LRCX.O), and Applied Materials Inc. (AMAT.O).

If we were to focus on the CHIPS and Science Act of 2022, it invests nearly $250 billion in semiconductor R&D—one of the largest funds provided for R&D in the United States. While the act aims to boost the semiconductor manufacturing capacity in the U.S., its goal is for the country to maintain its technological leadership, especially when considering the threat coming from China.

Regarding the U.S. export ban of advanced technology to China, it is important to state that the regulation focuses only on graphic processing units (GPU) such as Nvidia’s A100 and H100 chips, and AMD’s MI250 chips. These technologies are widely used for military systems as they are employed for image recognition or to carry out calculations quickly and with precision.

Taiwan is another important factor in the U.S. semiconductor policy. For some time, Taiwan has been a cause of conflict between China and the U.S. While the Taiwan issue is directly related to China’s national security interest, Taiwan, as discussed above, is important to the U.S. as one of its main sources for chips, and especially those used for military purposes. Thus, any possible intervention by China in Taiwan would threaten the U.S. semiconductor supply chain and, therefore, the U.S. economy.

At the same time, the situation between the U.S. and China seemed to escalate further in August 2022, when Nancy Pelosi, the speaker of the U.S. House of Representatives, visited Taiwan, despite China’s opposition.

What is more, a few days ago, Biden stated that the United States would defend Taiwan military if China were to attack the island. All these developments not only point to the existing rivalry between the great powers, but most importantly to the possibility of their technological decoupling. If this occurs, the implications will have a large impact on the current international order.

I don’t think this addition is very important as it is already stated in the sentence above if there is a possible intervention by China in Taiwan. Just is case I added a few words.

The United States’ national interests and the preservation of its position as sole hegemon remain at the heart of its semiconductor policies. The main problem for the U.S. is not only the production of semiconductors, but where they will be used. If U.S. dependency on China were to increase, so would the risk of China impacting the modernization and effectiveness of the American military.

Dependency on China would be detrimental to U.S. power: not only would it risk weakening the American economy and military, but it would also threaten the U.S.-led international order. The U.S. aims not only to strengthen and maintain its technological leadership, but also to weaken China’s rise, especially in technology.

Here it is useful to recall that while the U.S. has banned the export of several technologies (such as space technologies) to China before, similar steps were taken towards Japan in 1985 when the U.S. lost its leadership position in the semiconductor global market to the East Asian island country. As a response, among others, the U.S. imposed 100% tariffs on Japanese semiconductors, banned Toshiba products for three years, and requested Japan share its technologies.

The U.S., in fact, regained its leadership position, which continues to this day, while Japan’s position has declined considerably. It remains to be seen if the latest measures will affect China in the same way. It is certain, however, that the U.S. sanctions will push China further to focus on developing its own semiconductors—this may take time, but it is not impossible considering what China has achieved in a very short period of time. If this were to transpire, it would be a game changer and a true threat to the global leadership of the United States.

Gloria Shkurti Özdemir is a PhD candidate at Ankara Yıldırım Beyazıt University and writing her dissertation on the application of artificial intelligence in the field of military. Her research interests include U.S. foreign policy, drone warfare, and artificial intelligence. Currently, she is a researcher in the Foreign Policy Directorate at SETA Foundation and also working as the Assistant Editor of Insight Turkey, a journal published by SETA Foundation.

You can see how this popup was set up in our step-by-step guide: https://wppopupmaker.com/guides/auto-opening-announcement-popups/

![]()

Stay informed by subscribing to

our weekly newsletter.

You can see how this popup was set up in our step-by-step guide: https://wppopupmaker.com/guides/auto-opening-announcement-popups/

You can see how this popup was set up in our step-by-step guide: https://wppopupmaker.com/guides/auto-opening-announcement-popups/

You can see how this popup was set up in our step-by-step guide: https://wppopupmaker.com/guides/auto-opening-announcement-popups/

You can see how this popup was set up in our step-by-step guide: https://wppopupmaker.com/guides/auto-opening-announcement-popups/