Could Blockchain Be a Real Game Changer?

New-generation digital identities are about to replace conventional government-issued legal identity documents.

January 26, 2023

T

he four most important general-purpose technologies (GPTs) that have, so far, drastically changed humanity have been steam engines, electricity, information technology (IT), and artificial intelligence (AI). And contrary to what Mr. Gates argues, blockchain has just been added to that list.

Blockchain is a globally distributed public ledger technology. It enables a secure way of recording information as well as being a secure peer-to-peer method of verifying information, movement of assets, documents, and, in particular, real-time money transfer across the world economies. And it does so with significantly small costs due. It also provides transparency, decentralization, and increases efficiency and decreases transaction costs thanks to no intermediaries.

Although there were a number of similar technologies as late as the 1970s, the blockchain technology itself was first publicly introduced by the famous Nakamoto (2008) paper of Bitcoin, following the Global Financial Crisis of 2008. And today, almost all cryptocurrencies have their own blockchains as in the bitcoin or Ethereum blockchains.

Decentralization or the decentralized nature of the blockchains basically means that the validation process is not through a central authority, but rather via a consensus algorithm in a distributed network. It decentralizes digital records of products or information and is user verified. It also provides anonymity, without revealing the true identity of a user.

Fundamentally, blockchain helps deal with the trust issue. That’s why The Economist once called it the “trust machine.” This new mechanism of proving trustworthiness is particularly important for small and medium-sized enterprises (SMEs), startups, or individuals that don’t usually have a built-up reputation yet. One should not forget that the conventional financial system is also primarily built upon “trust.” And this is, in the meantime, a fundamental weakness (for conventional finance) considering the frequent financial distress periods.

Blockchain could be used in smart contracts in the shipping industry, in digitalizing the supply chains, payments, and in financing trade. Blockchain’s use in supply chain management, in business strategies, and in dealing with trust-related challenges as well as in security, privacy, payment, and settlement systems should be well-noted. It could help balance between cooperation and competition, and deal with modern issues of opportunism and adverse selection.

Its extensive use in finance is already popular. However, companies such as Maersk and Walmart have also been effectively using this new technology to decrease costs, increase quality, and facilitate their business processes. Smart contracts supported by blockchain technologies can increase efficiency by fastening digitalization and decreasing operational workload in conventional business models. They can provide transparency, speed, and security to all parties.

Third-party trust issues (related to intermediaries such as banks) are already addressed by the blockchain technology. However, how about first-party and second-party trust issues? Indeed, as rightly pointed out by Kshetri (2022), the combination of blockchain with the other technologies such as AI could help overcome the other dimensions of trust-related challenges as well.

The Fourth Industrial Revolution or Industry 4.0 (digital revolution) is of critical importance at this point as it can be used to increase the productivity and efficiency of the blockchain technology. The Industry 4.0 (digital revolution or IoTs) could be used to deal with the other dimensions of trust, and increase the productivity and efficiency of the blockchain technology.

Blockchain-based identities to replace missing legal identity documents are a key first step in the introduction of the blockchain technologies in many industries. An efficient and reliable property, house, or land registry system could be a huge plus particularly in underdeveloped economies. Developing sustainable supply chains is another critical contribution. For example, PWC estimates effective use of blockchain in SCM (supply chain management) could increase global GDP by almost $1.8 trillion by 2030.

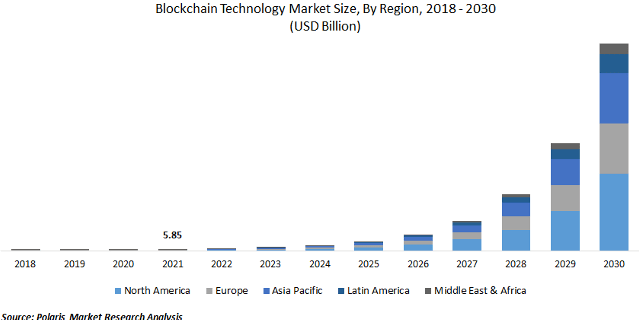

Blockchain technology attracts even more investment and venture capital as its use in finance, banking, cybersecurity, payments, and smart contracts increases. The global blockchain technology market was a little over $2 billion in 2018 and $5-6 billion in 2021, according to Polaris Market Research, PWC, and a few others. It is expected to exceed the $10 billion threshold in 2022. Between 2022 and 2030, on the other hand, it is expected to grow by 80-90 percent per annum, and eventually reach somewhere between $1.2 and $2 trillion. The Asia Pacific, including China and India, in particular, is expected to raise its share the most.

Blockchain helps create new networks, organizations, and models; functions as an intermediary instrument or authority of verification; and replaces the conventional trust instrument in any formal business relationship or business contract. Meanwhile, just as in the decentralized autonomous organization (DAO) example, blockchains are likely to lead to new business models and new-generation organizational setups.

Blockchain-backed decentralized and automated validation mechanisms can create new business models and new setups where you could even earn a passive income in an automatic investment scheme. A self-driving car, automated financial transactions such as paying bills or money transfers, loan applications, and access to low-cost capital could be also be enabled.

Real estate assets, which are heterogenous and immobile, are another example. The market is illiquid, localized, and highly segmented. High information asymmetries and room for private bargaining make it difficult for authorities to follow up on the transactions. High transaction costs due to the large number of trusted intermediaries and confirmation authorities is another issue here. This is, indeed, where blockchain steps in. And, these blockchain-based land records are particularly beneficial for developing economies.

Blockchain is mostly associated with finance and cryptocurrencies, as its first application was in the introduction and transfer of bitcoins. The fast and efficient transactions made possible by financial technology (FinTech) along with its ordering, payment, and settlement aspects increase its efficiency and attractiveness. Blockchain could even be effectively used in international money transfers and liquidity flows or remittance transfers, just as in the RippleNet (XRP) or Stellar Lumens (XLM) networks.

Decentralized finance (DeFi) is another good example of blockchain projects that aim to remove human involvement from financial services in order to make them cheaper, faster, and more inclusive. DeFi protocols are predominantly run on an Ethereum network. A key weakness of modern DeFi protocols, on the other hand, is that they miss an oracle, which is an independent, trusted third party.

Meanwhile, blockchain can also be used to improve security and privacy in finance, IoT devices, and even in healthcare. It will work much better than the conventional password-based security systems. In the health sector, at a minimum, people won’t have to send or record their personal data at some central repository; data won’t be sent over to anyone or anywhere, and just an access permission will be given whenever needed.

Blockchain will definitely help in gaining privacy in healthcare data, but not for those who are in need, such as the elderly and people with disabilities. However, it is still not clear whether blockchain would also replace credit scores, as a new mechanism of proving trustworthiness, by increasing transparency and mitigating the lending risk.

Security of IoT devices, cybercriminal activities, and data breaches could be avoided with the higher level of security of the blockchain technology. Blockchain technology is also used in many other industries including its application in insurance, government and public records; crowdfunding and venture capital; cybersecurity, agriculture, transportation, logistics, education, and even in politics and gaming.

Financial inclusion will also certainly be improved in countries where a large population does not have a bank account or access to financial services. For example, according to the World Bank Identification for Development (ID4D) global dataset, one billion people still do not have any form of identification. In China, only 20 percent of the population have a credit score. In Sierra Leone, only 2,000 people (out of 7 million) have a credit score. Up until 2011, just 35 percent of the population in India had a bank account.

That said, rather than the modern-day tulip bubble cryptocurrencies, blockchain-based central bank digital currencies (CBDCs) and digital tokens representing some tangible or intangible assets are the future of digital technologies in finance. A few of the benefits of these digital currencies and blockchain technology would be:

Recommended

One should also beware of potential risks, challenges, and security pitfalls of blockchain in the public sector and services. It should, for instance, not provide an escape from the regulations and laws of the states. Blockchain could even be an alternative tool or means of governance and legal identity, and potentially replace public verification mechanisms. This, however, should not undermine the rule of law.

Meanwhile, the lack of technical specialists with blockchain expertise is another critical challenge. There are already too many software developers, but too few of them are actually aware of the blockchain codes. Demand for software engineers and blockchain developers is rising by a few hundred percentage points per annum. The majority of blockchains, up to 60-70 percent, are also still running on relatively costly and slow Ethereum platforms, and major improvements are still required.

Blockchain-based financial technologies such as CBDCs also have their own disadvantages and weaknesses. For example, too many fund transfers towards digital wallets could weaken traditional banks and financial systems. Tougher identity verification mechanisms are required to prevent money laundering, and other illegal or illicit activities. Limit controls on the highest amount users can hold could be a solution, at this point.

The sources and reliability of the data are also crucial. As the number of users increase, blockchain systems may also get inefficient and more complex. Meanwhile, new-generation digital identities are about to replace conventional government-issued legal identity documents. For instance, the European self-sovereign identity framework (ESSIF), as part of the self-sovereign identity (SSI) idea, is another strategic implication of the blockchain revolution in the middle-to-long run. This should, again, not undermine existing regulations and the rule of law.

Despite all these weaknesses, though, the blockchain technology is still a real game changer.

Dr. Bagis has a multidisciplinary B.Sc. from ITU (2006), an Economics M.A. from Sabanci University (2009) and a Ph.D. in Economics from the University of California (2014). In addition to his academic career, he has had private sector experiences at various international and domestic companies and institutions. He has taught graduate and undergraduate level economics, math and finance courses at prominent universities including University of California Berkeley and Sabanci University. His analysis and working papers are published by various prominent institutions including SETA and SAM.

![]()

Stay informed by subscribing to

our weekly newsletter.